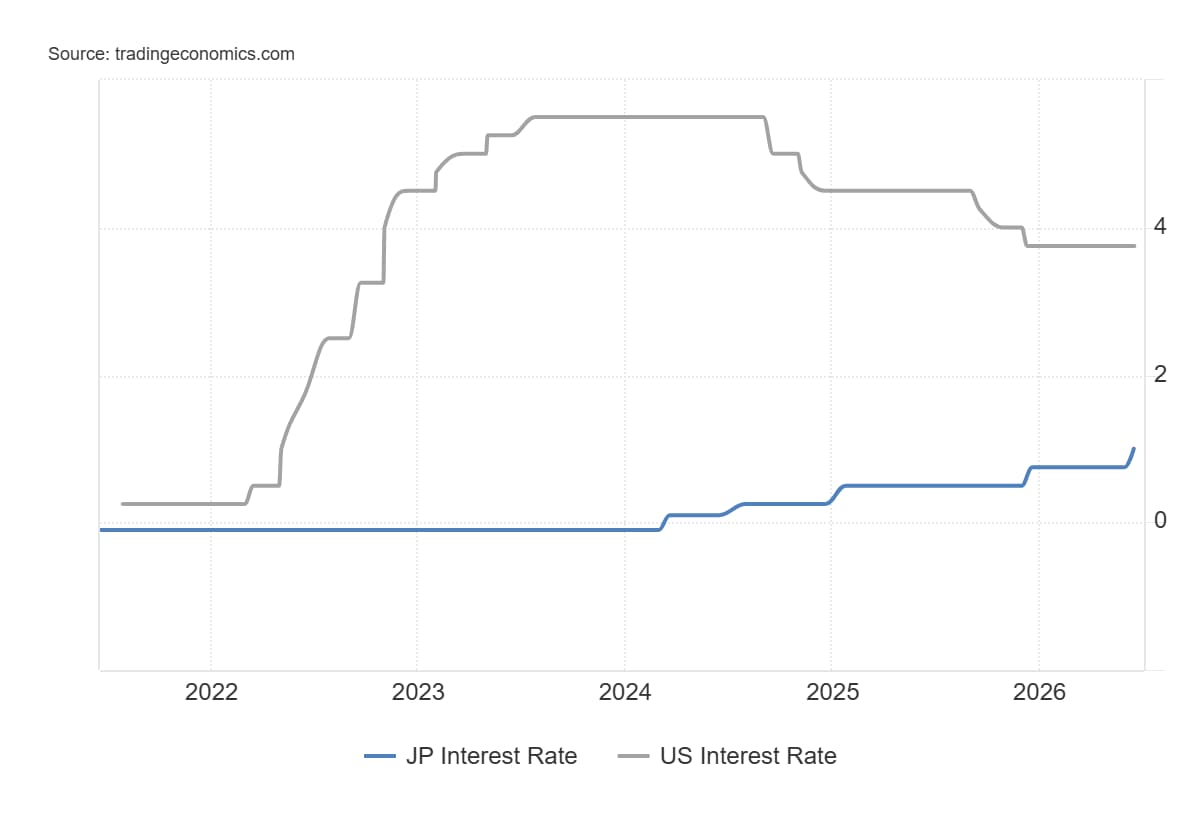

Japan may be changing its intervention playbook, but that might not be enough to rescue the battered Yen. With USD/JPY hovering at four-decade highs, the currency’s weakness is being driven less by speculative pressure and more by a powerful structural force: the wide US-Japan rate gap. BoJ hikes may slow the decline, but as long as the carry trade remains attractive, markets could keep testing how far Japanese authorities are willing to go.

Yen receives short-lived support from stealth intervention risks

Reports of a significant shift in Japan’s intervention tactics briefly bolstered the Japanese Yen last Thursday, though the market anxiety subsided amid the lack of concrete action, allowing USD/JPY to move back closer to a four-decade high.

Two sources familiar with the matter told Reuters last week that Japanese officials might shift away from their traditional approach of signaling FX intervention plans and instead focus directly on a campaign to squeeze speculators.

By abandoning explicit intervention warnings, Japan aims to keep traders guessing and raise the cost of betting against the JPY. This injected a new element of uncertainty and forced short sellers to unwind their positions.

Wide US-Japan rate gap keeps carry trade in play

The immediate market reaction, however, faded rather quickly as no official action has been confirmed yet. Moreover, analysts doubted that any such move might deliver lasting support to the JPY or alter the broader direction.

“The best policy for Japan is for the Bank of Japan to speed up its [interest-rate] hike frequency to let the market know it is becoming more active in supporting the Yen. And if that is not sufficient and the Yen falls further toward 165.00, FX intervention will be sensible,” said Takuji Okubo, chief economist of Japan Macro Advisors, Reuters reports.

Furthermore, the wide gap in borrowing costs between the US and Japan keeps the so-called carry trade active, wherein investors borrow in Yen at lower rates to invest in higher-yielding assets. Consequently, the resumption of JPY selling lifted USD/JPY to the 162.45-162.50 region on Wednesday.

“The Yen remains one of the market’s preferred funding currencies, which means every rally has to compete with the attractive returns available elsewhere,” said Vitalii Bulynin, CEO at Versus Trade. “Unless that dynamic changes, traders are likely to view Yen strength as an opportunity to rebuild their carry positions” he added.

Renewed US-Iran tensions add to JPY’s woes

Meanwhile, geopolitical volatility in the Middle East continues to threaten steady energy flows and is seen as another factor influencing exchange rate dynamics. The latest threats from US President Donald Trump, who said the interim deal with Iran is over, have revived fears of supply disruptions in the Strait of Hormuz just as markets were starting to price in a normalization of energy flows.

Japan relies on the Strait of Hormuz for over 90% of its Crude Oil imports, and supply disruptions through the strategic waterway remain a major threat to its economy.

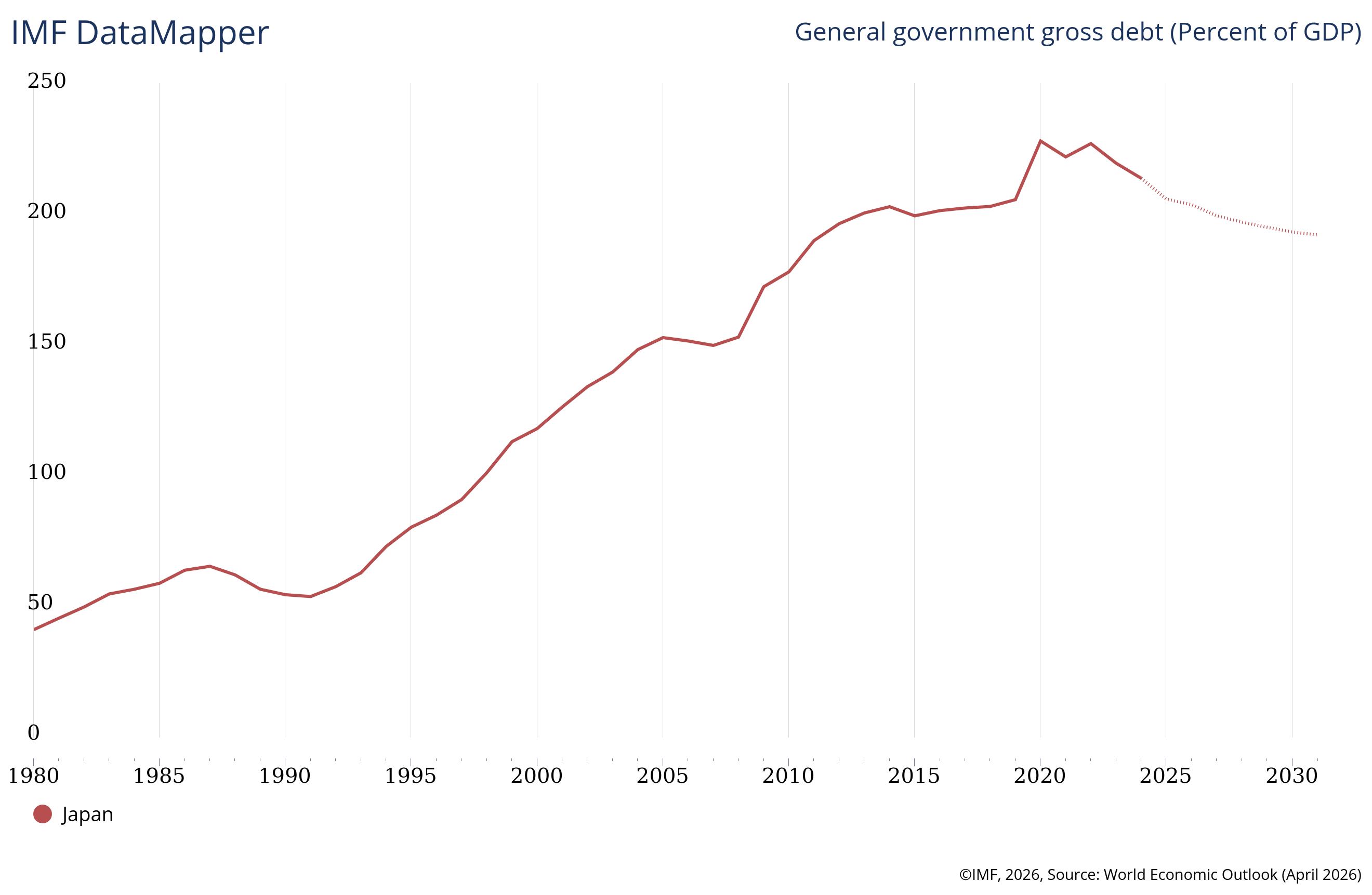

Japan’s fiscal concerns favor bears

Japan’s deteriorating fiscal health poses compounding challenges for the JPY and could further constrain any attempted recovery.

Since taking office in October, Prime Minister Sanae Takaichi has pledged to pursue a responsible and proactive fiscal policy. However, investors remain worried that the government’s expansionary spending agenda and changes to its fiscal targets could worsen Japan’s already strained public finances. Moreover, the uncertainty over how additional expenditures will be financed contributed to a sustained rise in Japanese government bond yields.

Rising yields are typically positive for the domestic currency, though it escalates the cost to issue and pay interest on deficit bonds. Moreover, fears that Takaichi’s pro-growth fiscal strategy will force the BoJ to keep monetary policy accommodative led to a decoupling between higher yields and a stronger currency. This suggests that any intervention would only act as a speed breaker and that the path of least resistance for the JPY remains to the downside.